The votes have been cast and now it’s a waiting game. Our country now faces days of a counting, recounting, accusations, potential lawsuits and a runoff election or two. Only then will we know the results of the 2020 election.

It can be hard for clients to keep emotions under control during an election season. Political views can affect how many see the world. After President Donald Trump was elected in 2016, the number of Republicans who said the economy was getting better rose from 16% to 49%. The number of Democrats went the opposite, falling from 61% to 49%. Yet, not much had happened economically in that short period of time.

Political views may also influence who our friends are. According to Pew Research, “Roughly 4 in 10 registered voters in both camps say they do not have a single close friend that supports the other major party candidate, and fewer than a quarter say they have a few friends who do.”

Historical Returns

Since the stock market often reacts to investor emotion, it’s not surprising that our political outlook can play a role. However, while unsurprising, it likely isn’t helpful.

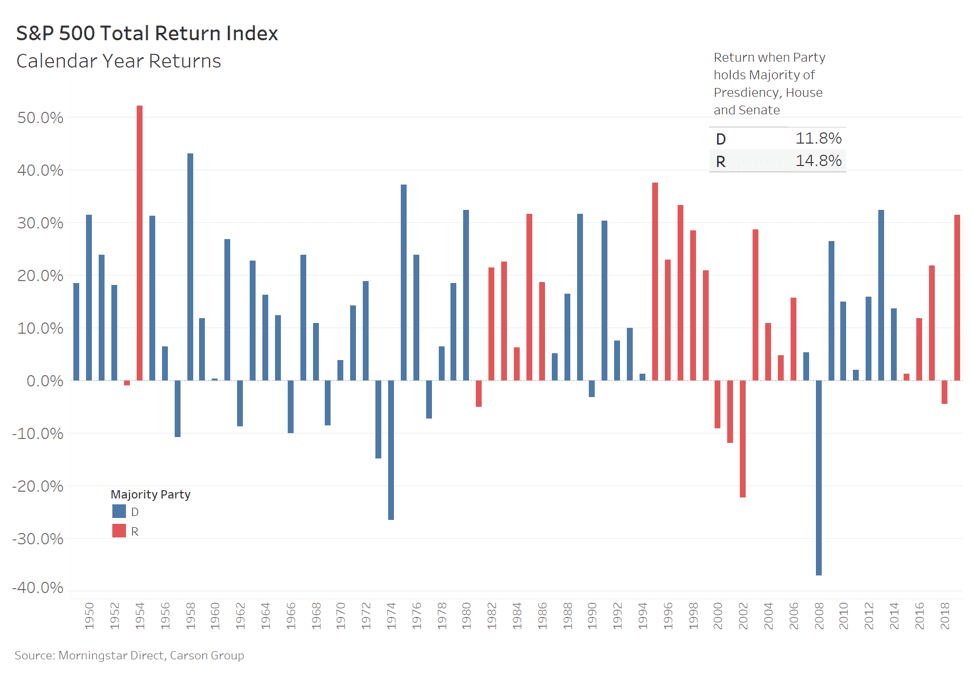

Based on data beginning in 1949, during periods when Republicans controlled at least two of the presidency, the Senate or the House of Representatives, the S&P 500 rose 14.8% per year. When Democrats held at least two, the S&P 500 rose 11.8% per year. When one party controlled all three branches, the average return was 15.0% while divided government averaged 11.5%. Both Democratic and Republican one-party control outperformed divided government, and Democratic presidents averaged a higher rate of return than Republican presidents.

The most important message to deliver to your clients is that stocks have gone up in the long run regardless of which party was in the White House or controlled Congress. In addition, there just isn’t enough data to support strong conclusions that political affiliation had a direct impact over the long-term. For example, there were 70 years that Republicans controlled two of the three governing bodies, and since the House is elected every two years, that means there were only 35 Congresses.

It’s also important to recognize that issues a client may care most about may not affect their portfolio very much. For example, while immigration, the Supreme Court and gun control can be highly contested issues during a presidential campaign, none play a large or direct role on the performance of portfolios.

2020 Analysis

For issues that do impact investments more directly, circumstances are likely to constrain what the candidates can accomplish.

- The launch and distribution of an effective vaccine and other progress against COVID-19 is likely the most direct path to improved economic growth. Neither candidate can make anyone go to a restaurant, attend a conference or board an airplane when the virus is not contained.

- The weak economy and an energized political opposition will limit the opportunity to raise taxes by a potential Joe Biden administration. Corporate taxes may increase but are unlikely to be restored to previous levels. In an economy struggling for growth and needing to find jobs for the unemployed, generating jobs will take precedence over additional revenue.

- Trade policy with China will remain a contentious issue, but both parties hold similar views. President Trump has been largely successful in adjusting how Americans see China. Of Republicans, 72% view China negatively, and 62% of Democrats hold the same view.

- The lack of a follow-up to the CARES Act has increased the focus on the next aid package. Both parties favor getting aid to Americans. The difference has been on the dollar amount and level of benefits to particular groups. Based on the results available on election night, Republicans are favored to retain the Senate. If this result holds, the size of the next aid package will likely be between $500 billion and $1.5 trillion. The package will target damaged industries, testing and some additional unemployment support. Aid to state and local governments and the level of additional unemployment support will be smaller than in a unified Democratic government. Meanwhile, differences between the current administration, Senate and House created a political impasse that has delayed the passing of additional economic stimulus.

- A Republican-controlled Senate also has the potential to reduce the degree of any tax increases that are proposed.

- It’s important to listen to your clients in this highly emotional time. However, there is danger in trying to adjust a portfolio based on election results. As the news changes, markets will react quickly to new information. The day after the election, growth stocks soared, small caps were flat and interest rates dropped. As odds of divided government grow, markets quickly reflected expectations for a smaller stimulus bill by reflecting lowering long-term interest rates and expecting a narrower recovery benefiting companies with a greater reliance on technology.

The market reaction shows us that election uncertainty isn’t shaping the markets as much as the fight against COVID-19 and company fundamentals. Markets didn’t plummet and the process goes on. Even if slow vote counting and election challenges slow the process further, the long-run focus will revert to something other than politics.

Key Takeaways

- A financial plan isn’t built on the idea that a Republican or Democrat will always be in the White House.

- The market is driven more by fundamentals than politics. The S&P 500 earned 12.5% annually from the day President Obama was elected until President Trump was elected. From Trump’s election through October 13, 2020, the S&P has returned 14.3%. For the politically motivated, the odds are one of these wasn’t your favorite president. Yet, stocks did well under both administrations.

- Help clients keep politics out of their portfolio. Just because an issue is important to an individual, it doesn’t mean it is to their portfolio.

—

Date prior to 1971 uses the S&P 500 (1936) TR Index. From 1971 on it uses the S&P 500 TR Index.

The views expressed in this material are the views of Scott Kubie through the period ended October 14, 2020 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements.